Graphite Electrodes is an indispensable part of steel making through the EAF route – and it’s evolving all the time in China. In tandem with Needle Coke quality improvements opening up previously unimaginable trade possibilities.

SteelMint with delegates from world over hit the road in China to find out all this and more. We immersed ourselves in the production processes and the plant visits helped us clear long-standing doubts.

China has emerged as the epicentre of the global Graphite Electrode (GE) market as it has the potential to shape global GE demand, prices and trade dynamics. In end-2017, the clampdown on 300,000 tonne of inefficient GE capacity in China triggered severe GE shortage across the globe, which further pushed prices upwards, even as steelmakers scrambled to secure supplies. However, the significance of recent announcements of capacity enhancement in China has been grossly downplayed by a section of the industry, with the prevailing opinion being that Chinese plants, inexperienced newcomers as they are, can’t manufacture UHP electrodes as they do not have the required high-specification needle coke.

Some of the unanswered questions crowding the minds of industry insiders have been:

- What is China’s GE and needle coke performance potential?

- Does Chinese GE and needle coke quality match global standards?

- Is the needle coke manufactured in China ideal for UHP grade production?

- What is the current expansionary state of EAF steelmaking in China?

Despite these pressing queries, the outside world still lacks a coherent understanding of the Chinese GE market. While traders and manufacturers around the world are eager to secure comprehensive, first-hand, ground-zero know how of the Chinese market, their channels of accessing such vital information were, unfortunately, clogged. This bleak scenario, however, used to prevail before SteelMint organised the novel and pleasantly offbeat International Graphite Electrode & Needle Coke Roadshow from 8-12 April, 2019 that included extensive tours of GE and needle coke plants in the country to assess the ground reality. The foremost objective of this tour-de-force of an event was to facilitate interaction between Chinese GE manufacturers and the outside world and to bridge the information gap pertaining to the Chinese GE industry.

Albeit hectic, the event shone a light on the Chinese GE and Needle Coke market and offered a non-blinkered insight into what the future holds. Here are the key takeaways from the Roadshow:

China’s GE Production Rising Fast

Since 2018, the supply of electrodes from China has started to increase. Supply is expected to expand sharply due to new facility investments in 2019 and 2020. In 2018, about 700,000 tonne of GE was produced contributing to a rise of 19%. In 2017, production increased by 16% compared to the previous year. The largest new plant is Baofang Carbon Material Technology, a joint venture between Baosteel Group and Fangda Carbon. It is scheduled to start operations in Lanzhou in 2020 with a nameplate capacity of 100,000 MTPA UHP electrodes.

Inner Mongolia Emerging as a GE Hub

With favorable investment policies and low electricity prices, the Inner Mongolia region is emerging as China’s GE hub, with production slated to reach 300,000 tonne this year plus an additional 100,000 tonne in 2020. In 2018, there were about 220,000 tonne of production plans in areas outside Inner Mongolia, but was postponed to 2019. One of them, Baoshan Changdu (40,000 tonne) has started production in Yunnan Province from February.

Chinese Producers Aggressively Improving GE Quality

Chinese GE producers are making constant efforts to procure quality needle coke either via imports or through domestic procurement as well as securing technology for quality improvement. Chinese electrode manufacturers are also focusing on producing more of UHP grade GE and that too of sizes higher than 700mm.

China Market Dominated by Small Diameter Electrodes

China’s EAFs and refineries are mostly small, with capacities of 50 tonne, essentially dominated by HP and UHP grade manufacturers of sizes under 500mm. More than 200 companies produce electrodes. In particular, it is estimated that there are more than 160 companies in Handan Area, Hebei Province, that specialize in processing and trade. Most companies often produce and sell second-grade electrodes on a very small scale with fake brands, thereby stoking quality concerns.

Global Non-UHP Grade GE Supply Might Rise

Chinese GE manufacturers are aggressively increasing the production of HP/RP grade electrodes and amid limited domestic demand they are focusing on exports. With removal of anti-dumping duty on GE imports to India, it is slowly becoming one of the favourite GE export destinations.

GE Prices in China Likely to Remain Stable

In 2018, the utilization rate of Chinese electrode companies was less than 60%. The expansion of existing suppliers, emergence of new companies and winter production cuts brought down electrode prices in the latter half of the year, subsequently affecting companies’ profit margins. In fact, in Feb 2019, the electrode prices in China fell by 17-20% due mainly to extremely sluggish demand during the New Year holidays. The EAF utilization rate was less than 5% and electrode stocks rose by 27% in preparation for delivery. However, given the fact that domestic as well as imported needle coke prices are surging, electrodes prices are unlikely to fall further in the coming months.

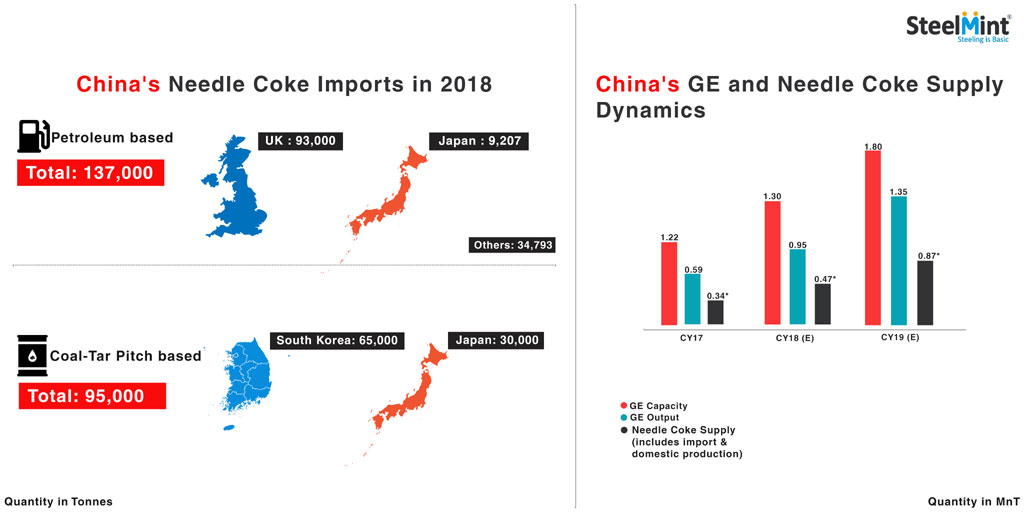

China’s Needle Coke Demand-Supply Imbalance

Needle coke imports and domestic production make up for 870,000 tonne in China whereas demand is 940,000 tonne, resulting in demand-supply imbalance. This apart, a majority of needle coke plants in China are pitch coke-based and high-quality coal tar pitch-based needle coke as well as petroleum-based needle coke still need to be imported.

Needle Coke Demand from Lithium-ion Battery Segment Growing

The demand for lithium-ion batteries in China is expected to grow at a rapid pace due to increased demand for new energy vehicles, as well as accelerating demand for energy storage batteries for on-grid and off-grid applications. The country’s needle coke demand from the ion-battery segment is surging. It is anticipated that China will have about 1 MnT of total needle coke capacity by 2020 out of which a substantial portion will be dedicated to the lithium-ion battery segment.

20% Rise in China’s EAF Capacity

As per market sources, China, which has increased its EAF steelmaking capacity from 6% of total annual production in 2016 to 12% in 2018, is likely to increase EAF steelmaking to 20% of overall crude production by 2025. Regardless of the forecast, virtually all EAFs in China are meant for production of special and stainless steel, while carbon steel accounts for only 60-70% at the moment. Also, low price competitiveness compared to BFs might stall EAF capacity enhancement. GE demand, therefore, will likely soar in the near- and mid-term.

The International Graphite Electrode & Needle Coke Roadshow organized by SteelMint offered a rare and holistic insight into the Chinese GE industry that market watchers from across the world are tracking attentively. However, market participants who were eager for a direct interaction with Chinese GE and needle coke bigwigs but have unfortunately missed the bus this time around need not lose heart. Not all good things in life come just once. A golden opportunity that slips between the fingers elicits regret but there is always a second chance to look forward to in intense anticipation. Take heart.

Industry insiders who could not join the SteelMint Roadshow but are anxious to catch up on precious bits of latest information on the Chinese GE market ought forthwith book their seats at the 2nd Global Graphite Electrodes Conference to be held in Bangkok, Thailand’s Hotel Avani Riverside from August 27-29.