MRAI is organizing its 2nd Edition of Business Summit (1st to be held Internationally) on 21 & 22 August 2023 in Hotel Bangkok Marriott Marquis Queen’s Park. MRAI Business Summit will bring Indian and International Recyclers together for Networking and showcasing their business interests, products, technologies, services, new innovations, perspective, etc. under the one roof. Conference will accommodate 500+ Delegates, 6 Diamond Sponsors and 24 Exhibitors representing Recycling Fraternity on first come first serve basis.

Who Should Attend:

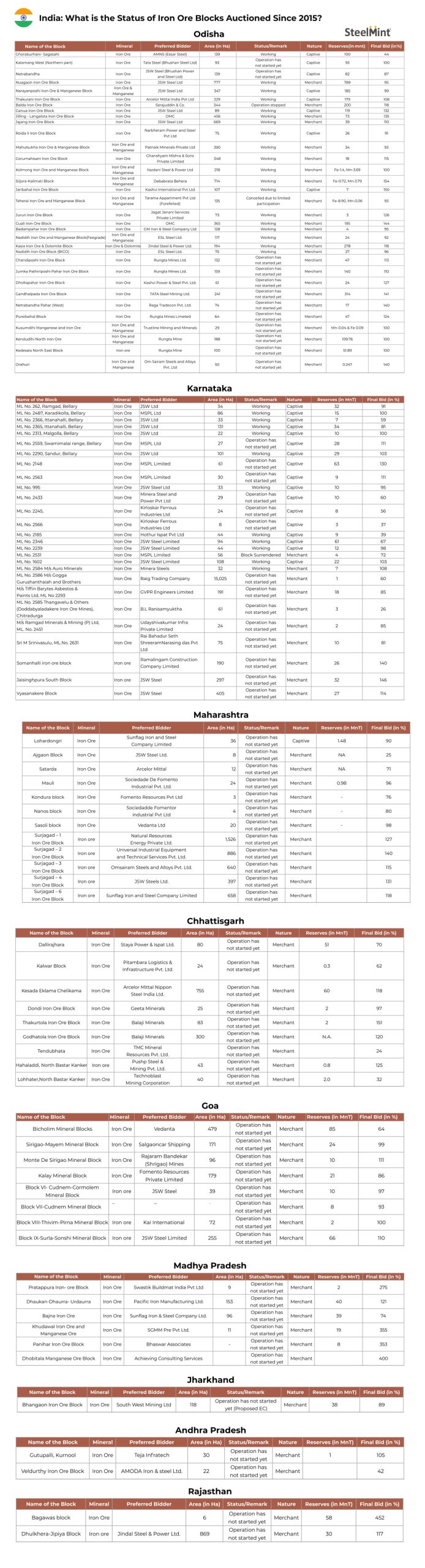

Around 100 iron ore mine blocks have been successfully auctioned in India since the historic amendment of the Mines and Minerals Development & Regulation Act (MMDR Act) in 2015, as per SteelMint data.

MMDR Amendment: Key facts

The landmark MMDR Amendment Act, 2015 paved the way for the introduction of the auctions regime in India’s mining and minerals sector by replacing the older first-come-first-serve system in a bid to ensure transparency in allocation of mineral blocs.

The reforms undertaken in 2015 have resulted in successful auctions of 273 mineral blocks in different states of the country since 2016. Importantly, the pace of mineral auctions has quickened since the MMDR Amendment Act of 2021, with around 105 iron ore blocks getting auctioned in FY’23.

This has been possible due to radical reforms in the 2021 Amendment such as the abolition of the ‘end-use’ restriction for auctions and uninterrupted transfer of valid old environmental clearances to the preferred bidder.

It bears recall that the 2015 MMDR amendment had set forth specific clauses as regards renewal of mine leases. While merchant mines had their leases extended till 2020, the captive iron ore mines were given a timeline till 2030 after which those mines must come under the auction hammer.

In order to augment domestic iron ore supplies, Section 8(A) of MMDR Act was further amended allowing any lessee of a captive mine to sell minerals up to 50% of the total mineral produced in a year after meeting the requirement of the end-use plant linked with the mine. This, however, would require an additional amount to be paid to the concerned state government.

Similarly, government companies or corporations whose mining leases have been extended after the commencement of the MMDR Amendment Act, 2015, shall also pay such additional amount for the mineral produced after the commencement of MMDR Amendment Act, 2021.

The additional amount for extension of mining leases is 1.5 times the prevailing rate of royalty for iron ore mines.

Auctioned blocks

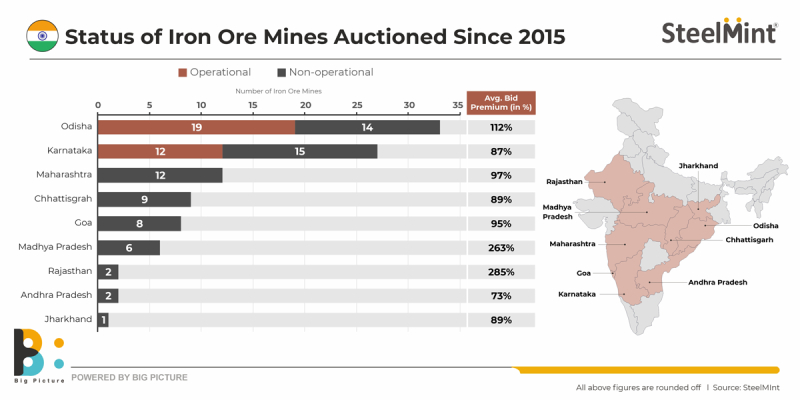

Notably, out of the 100 iron ore blocks auctioned thus far, 33 are in Odisha and 27 in Karnataka – India’s leading iron ore producing states. Among the other key producers, 12 blocks are in Chhattisgarh, 9 in Maharashtra and 8 in Goa.

Details of auctioned blocks

There are blocks in Madhya Pradesh and Andhra Pradesh, too. However, major iron ore-producing-state Jharkhand has just one block. A lion’s share of that state’s iron ore production is accounted for by captive steel producers.

In an indicator of over-enthusiastic participation in iron ore auctions – mainly by steel players eager to secure long-term supplies in view of surge in capacity – the general average auction premium quoted stands at over 100%, as per SteelMint estimation.

Outlook

India’s iron ore production in FY’23 inched towards 260 million tonnes (mnt). Out of the auctioned blocks, just over 30-odd are in working status which shows that many more mines – especially those auctioned since 2021 – will move towards operationalisation sooner rather than later.

Therefore, SteelMint’s outlook is positive as regards iron ore production even as domestic steelmaking capacity gathers pace.

What are the key government policies that may reshape the Indian minerals industry and how long might high premiums sustain for mineral block auctions? Gain cutting-edge insights from experts on these issues and much more at SteelMint Events’ flagship 6th Indian Iron Ore & Pellet Summit to be held from 24-26 August at JW Marriot, Kolkata.

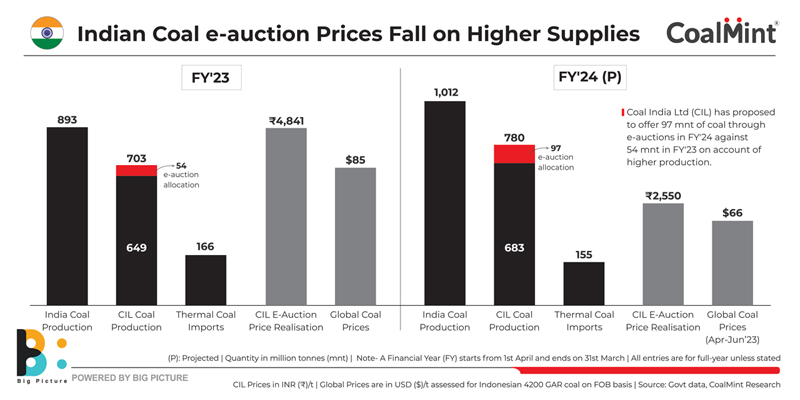

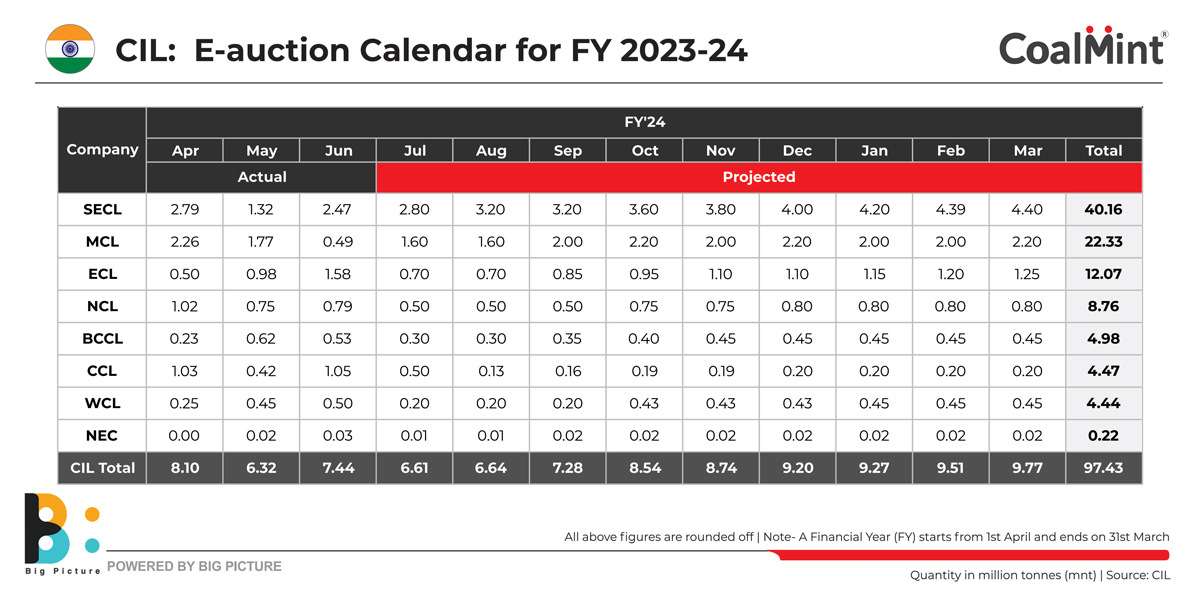

State-run miner Coal India Ltd (CIL) has floated a calendar outlining the proposed coal volume to be offered under e-auctions during FY’24. The company is planning to sell 97.43 million tonnes (mnt) of coal, which is around 81% higher than 53.91 mnt offered last year of which 52.88 mnt was booked.

As per policy guidelines, CIL earmarks 10% of its annual production for sale via regular e-auctions based on competitive bidding, whereas the majority of the sale is carried out via fixed price contracts under fuel supply agreements (FSA).

However, the company has been skewing this norm by regulating the coal offering based upon availability. This year, it has allocated a higher volume for e-auction than the actual norm, based on the projected production of 780 mnt, in view of supply-side improvements.

The auction calendar highlights that CIL has already offered 21.86 mnt of coal in the first quarter (April-June’23) registering an exponential growth of 115% compared to the year-ago period. The remaining 75.56 mnt will be sold in phases during the final nine months.

There was also indication of reduced offerings in July-August against June levels on account of expected supply disruption during monsoon. From then on the offered quantity rises progressively on a monthly basis in tandem with the increase in production, with total tonnage peaking in March.

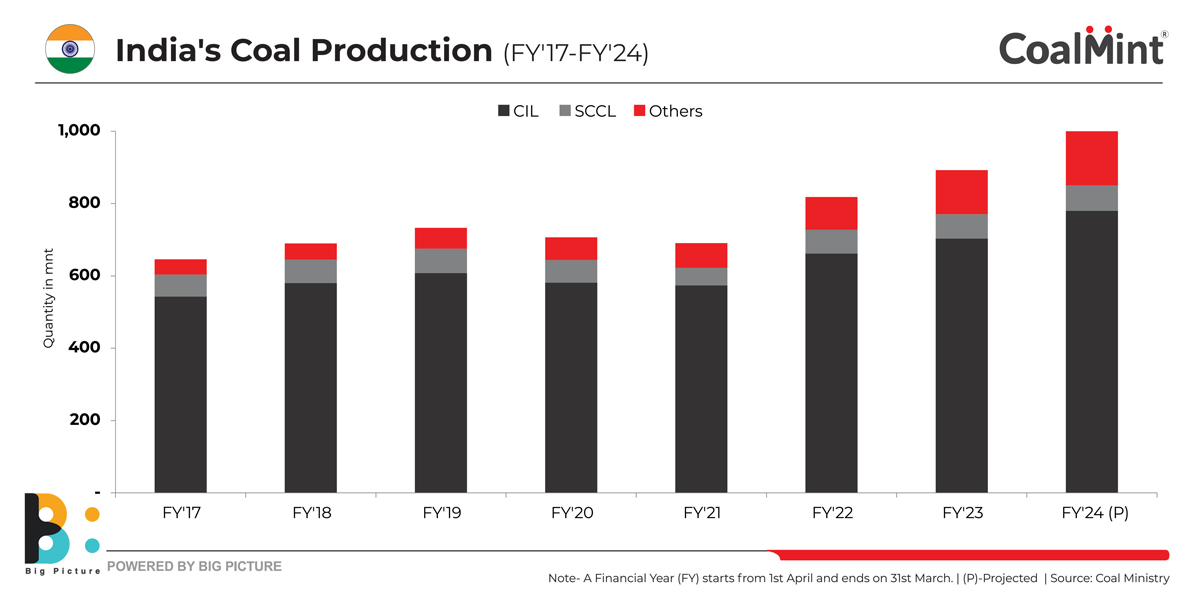

Production to breach 1 bnt-mark

The government has set a coal production target of 1,012 mnt in FY’24. Of this, CIL’s share has been fixed at 780 mnt, while Singareni Collieries Company Ltd. (SCCL) is expected to contribute 80 mnt. The remaining volume of 162 mnt is expected to come from captive and commercial miners.

In particular, CIL has set sights on creating a new production milestone by surpassing the previous high of 703 mnt attained last fiscal.

In Q1FY’24, CIL’s production jumped 10% y-o-y to 175.5 mnt, which is the highest ever production recorded during Q1 of any fiscal year. Dispatches increased 5% y-o-y to 187 mnt in Q1, which was around 7% higher y-o-y.

The performance trend indicating sharper production growth relative to dispatches has reduced inventory liquidation at mine level. This has helped the miner to accumulate sufficient inventory and also provide a leeway to increase e-auction volumes.

Besides, substantial growth in contribution from captive and commercial miners also provides new avenues for buyers thereby augmenting domestic availability.

Recovery in global supplies

In the aftermath of the Russia-Ukraine war when disruption in trade flows had triggered an unprecedented surge in coal prices, the Indian government was forced to take necessary measures to ensure fuel security at power plants.

This also forced CIL to curtail its offerings via e-auctions and resort to diverting the additional tonnage meant for sale in order to increase supplies to power plants.

However, as global supply pressure eases, there is adequate material availability for the imported coal-based plants which has also gradually reduced the pressure on domestic coal-based power plants.

Subdued coal-fired power generation

On the demand side, nominal growth in coal-based power generation owing to favourable weather conditions has also reduced the burden on domestic miners.

As per data provided by the Ministry of Power (MoP), coal-based power generation grew 2% y-o-y to 315.3 billion units (BU) in Q1FY’24 against 308 BU in Q1FY’23. Last year, the growth in generation volume at this juncture was around 20%.

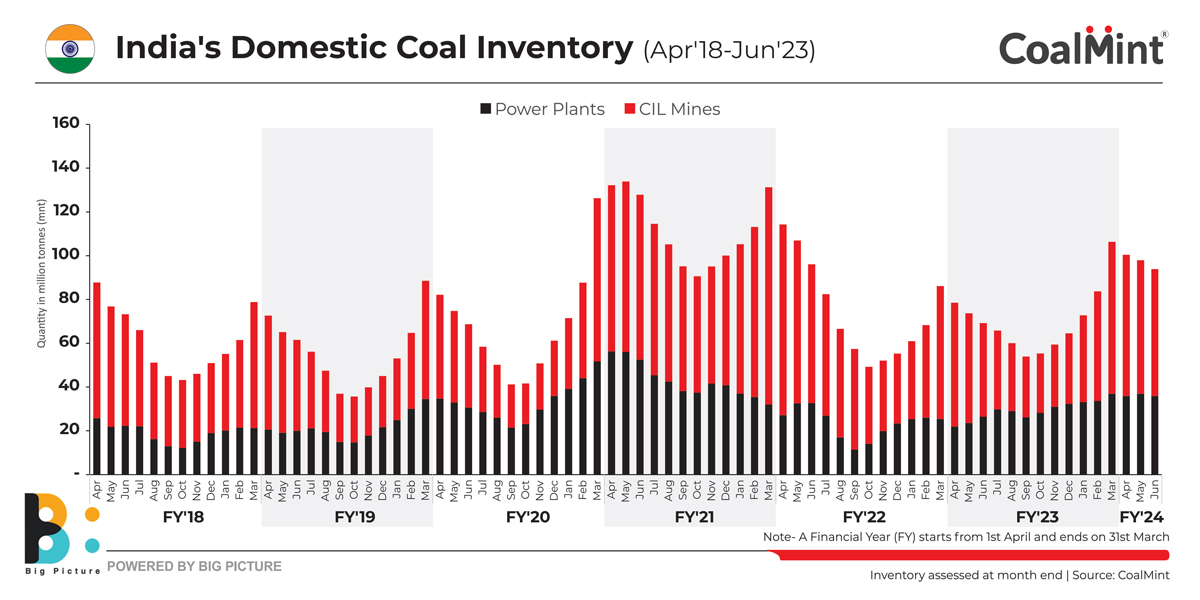

Rising stockpiles

While, CIL has accumulated sufficient inventory at mine pit-heads, the power plants have also shown encouraging signs with regard to inventory build-up aided by higher supplies and subdued generation.

Coal inventory at power stations was assessed at 35.88 mnt towards the end of June, which is sufficient for 13 days of power generation. Besides, the number of plants having a critical stock position has reduced to 61 currently from 87 in the year-ago period.

In all, combined inventory at CIL’s mines and power plants has increased to 93.9 mnt in June, up 36% y-o-y.

Outlook

The uptick in e-auction volumes is expected to push coal prices lower which are already reeling under the impact of improvement in supplies both at the domestic and global levels.

CIL’s price realisation for e-auction sales has dropped nearly 40% to INR 2,950/t in the June quarter from INR 4,841/t recorded in FY’23. Prices are expected to inch down to INR 2,550/t in full-year FY’24.

There seems to be minimal impact on imports from increased e-auction sales as Indian buyers are reaping benefits of ample material availability at cheaper prices. Presently, thermal coal imports on a monthly basis are assessed at around 16-17 mnt in Q1FY’24 against the average of 14 mnt in FY’23.

However, in a scenario where there is not much improvement in demand, lower e-auction prices may reduce imports which are expected to drop to 155 mnt in FY’24 from 166 mnt in FY’23.

3rd India Coal Outlook Conference

How will CIL’s altered auction dynamics affect domestic buyers? Supplies to the non-regulated sector rose 34% in FY’23 –will the trend continue in FY’24? To hear experts deliberate on these topics and much more, register for SteelMint Events’ 3rd India Coal Outlook Conference to be held at JW Marriott, Kolkata, from 24-26 August, 2023.

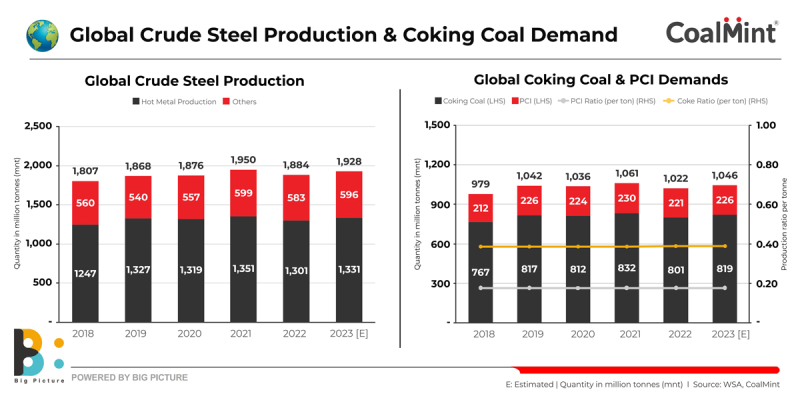

Global demand for coking coal in steelmaking is expected to increase by around 2.25% y-o-y in 2023. World Steel Association’s (WSA) short-range outlook published in April this year predicts that world crude steel production is expected to increase by 2.3% in 2023 from 1.88 billion tonnes (bnt) last year to 1.92 bnt.

Therefore, CoalMint estimates that global coking coal demand is likely to reach around 819 million tonnes (mnt) this year from roughly 800 mnt in 2022. Data reveals that global coking coal demand (excluding PCI) has grown nearly 7% since 2018.

WSA data shows that the share of oxygen steelmaking (BF-BOF) in global crude steel production was over 71% in 2022, with the rest being accounted for by the electric route (predominantly EAFs and also IFs). Therefore, global hot metal production in blast furnaces is expected to be around 1,331 mnt (1.331 bnt) in 2023–an increase of over 2% on the year from 1.301 bnt in 2022.

Demand for PCI

Notably, total coking coal demand must also include pulverised coal injection (PCI) used in blast furnaces to accelerate the process of reduction. Demand for PCI coal is likely to inch up to 226 mnt in 2023 from 221 mnt last year. So, total global consumption of coking coal + PCI may rise to 1.04 bnt this year from 1.02 bnt in 2022, as per CoalMint estimates.

Estimates further show that while the average usage of metallurgical coke in blast furnaces is at the rate of 390 kg per tonne of hot metal, the PCI rate per tonne of hot metal is 180 kg. These figures represent the global average. However, many companies have increased PCI use in the BF by as much as 250 kg per tonne of hot metal and this is mainly a cost-cutting measure. Roughly, 1 tonne of PCI replaces 1 tonne of coke and 1.5 tonne of coking coal is required to produce 1 tonne of coke.

Trade & price outlook

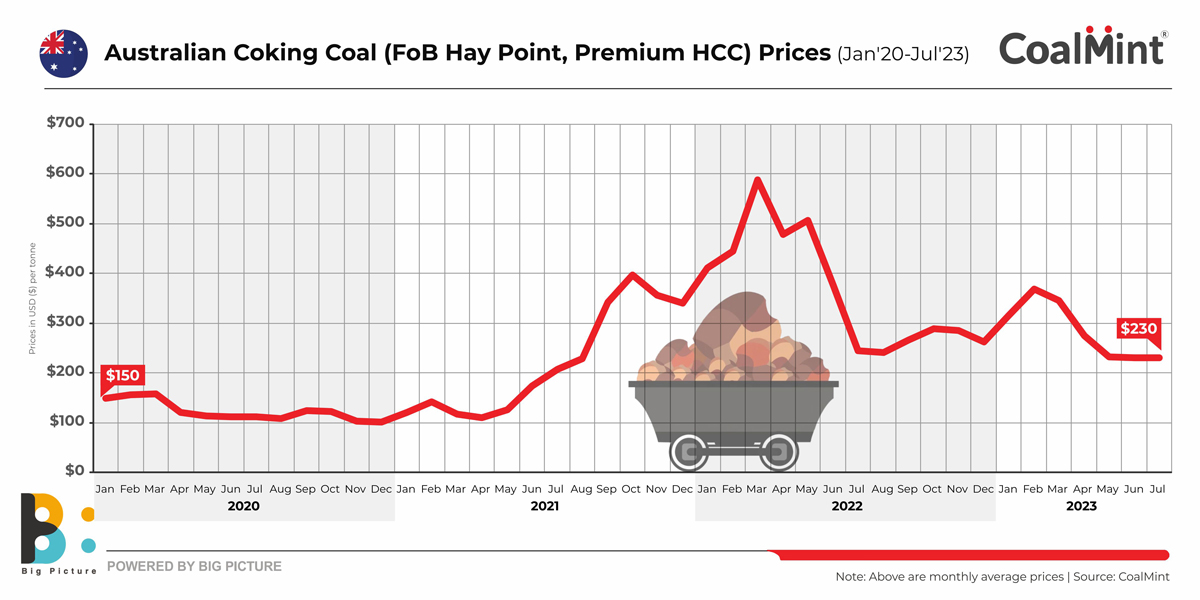

Australian premium coking coal prices have decreased to $230/t FOB from $300/t in mid-March 2023. Global inflation, monetary tightening, energy market volatility have impacted the steel market adversely. Below are factors which may impact prices in H2CY’23:

The extent of steel production curbs in China in H2 weighs on market sentiments and also obviously on coking coal demand. China accounts for roughly 56% of global steel production and 18% of seaborne coking coal demand. It is also the biggest spot market for met coal. Australian government sources predict that China’s imports of seaborne coking coal may drop 20% y-o-y in 2023.

Steel production in India rose over 8% y-o-y in Q1FY’24, as per JPC data. Steel demand is expected to increase by over 7% this year and production is likely to grow by over 10%. Commissioning of new blast furnace mills is surely positive news for coking coal demand. Sources are of the view that prices should revolve between $225-245/t FOB in H2.

According to the Australian government’s Department of Industry, Science and Resources, almost 15 mnt of blast furnace capacity has come back online again in Europe, as the continent has been able to effectively battle energy inflation. So, coking coal demand will remain largely stable in H2.

Weakening global steel market sentiment and its impact on exports weigh on the Japanese and South Korean steel industries. The two countries have a combined share of 27% of global seaborne imports. The recovery in manufacturing and automotive supply chains is an upside; however, demand outlook is largely stable.

Higher supplies are expected to weigh on prices in H2. Australia is ramping up shipments with the end of the La Nina climate episode. Supply outlook from the US and Canada is largely unchanged barring some disruptions in the US. Russia has diverted a portion of its cargoes to Asia, while Mongolia is looking to increase supplies with the laying of new railway networks.

Thermal coal prices have fallen sharply and the incentive to sell coking coal in the thermal coal market is lacking currently unlike last year. So, supplies will increase further and exert pressure on prices.

3rd India Coal Outlook Conference

Hear experts deliberate on ‘Global metallurgical coal & coke market trends: Will supply concerns intensify?’ at SteelMint Events’ 3rd India Coal Outlook Conference to be held at JW Marriott, Kolkata, from 24-26 August 2023. Register now.