-

Strong emphasis being given to solar energy

-

Setting up of fresh coal-fired plants banned

-

More hydropower imports from Nepal planned

Bangladesh, a key South Asian player in the steel manufacturing and ferrous scrap import space, is taking a proactive multi-pronged approach in its power sector to reach its emission targets.

It is not only encouraging renewable energy (RE) expansion but has banned further setting up of coal-fired power plants.

As per Climate Watch data, Bangladesh’s greenhouse gas emissions nearly doubled in 2018 from a decade ago although it remains a small emitter at a global level.

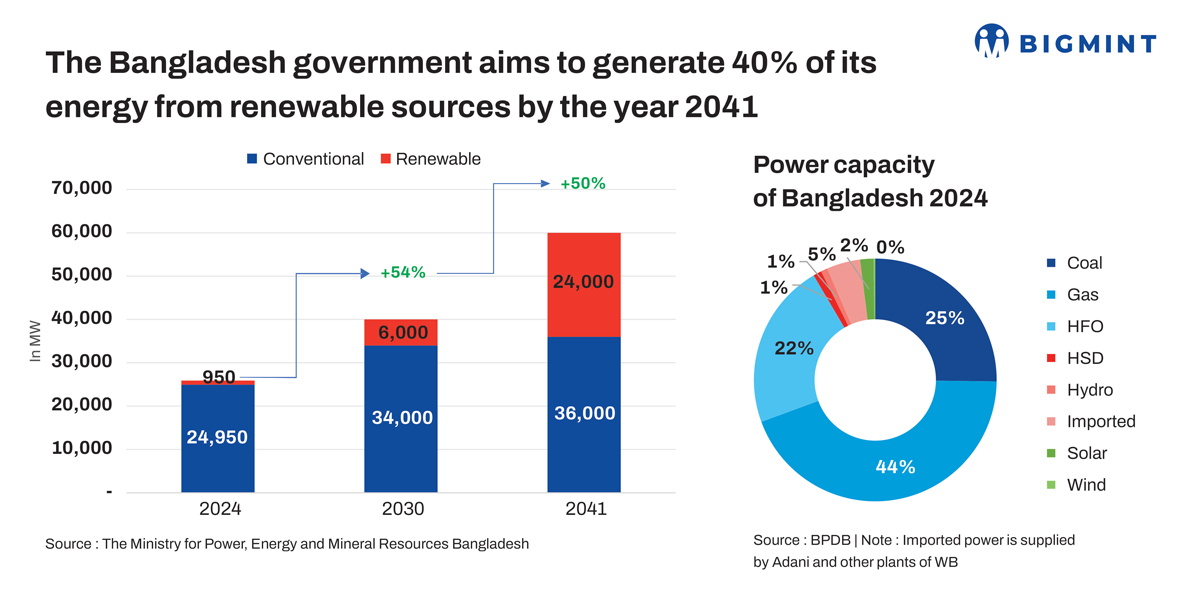

Its Ministry of Power, Energy, and Mineral Resources announced a few years back that Bangladesh aims to generate 40% of its electricity from clean energy sources by 2041, a key component of the country’s long-term strategy for the power sector.

State Minister for Power, Energy, and Mineral Resources, Nasrul Hamid, outlined that this plan involves importing about 9,000 MW through regional cooperation with neighboring countries.

Additionally, the government has set a target to derive 10% of the total power generation from renewable sources by 2041. Currently, Bangladesh’s power generation capacity stands at 25,826 MW, with 1,160 MW being imported, mostly through hydropower from Nepal and Bhutan.

The installed capacity of renewable energy in Bangladesh has risen to 950.72 MW.The government is confident in achieving a power generation capacity of 40,000 MW by 2030 and 60,000 MW by 2041, with a significant focus on renewable energy and regional energy cooperation.

Current power sector scenario

Bangladesh has an installed capacity of around 26,000 MW while its actual generation comprises around 14,300 MW.

Its power demand varies according to season. In summer, the peak demand season, consumption hovers around 16,000-18,000 MW. Winter, the lean period, sees demand dropping to 9,000-10,000 MW.

Within the 14,300 MW of current demand, the major chunk of 30-40% is contributed by gas-based power generation while 20-25% is coal based, 18-20% is HSFO (high sulphur fuel oil)-based, and the balance 3-5% comprise of renewables.

But, due to higher tariffs, HSFO-based power plants are not being encouraged by the government.

Gas-based plants contribute the highest to power generation essentially because of their comparatively higher efficiency level. The country sources locally from its own gas fields. The deficit in LNG is met through imports from the Middle East and Singapore. At present, the total LNG requirement is 3,500 MMcfd with which domestic production amounts to 2,700 MMcfd and the balance 800 MMcfd are imported.

HSFO-based power generation comprises around 7400 MW. But tariffs here are quite high compared to gas or solar.

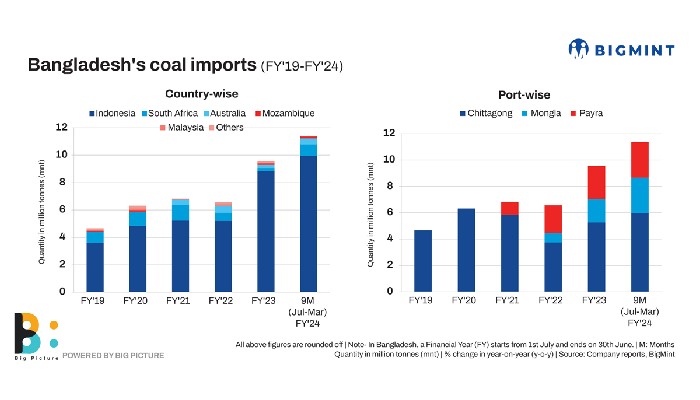

While the bulk is contributed by gas, the share of coal-fired generation has been increasing steadily since 2019.

According to Bangladesh Power Development Board (BPDB) official statistics, new power plants that are either already connected to the grid or are in the process of being linked will contribute significantly to the energy supply. The additions include:

- 1,600 MW from Adani Group’s coal-fired power plant

- 620 MW from the Rampal Power Plant

- 1,224 MW from S Alam Group’s coal-fired power plant in Bashkhali, Chittagong

- 718 MW from Reliance Power’s LNG-based plant in Meghnaghat

- 590 MW from GE-Summit Meghnaghat-2’s LNG-based power plant

- 584 MW from Unique Group’s LNG-based power plant, also in Meghnaghat.

These new power sources represent a diverse mix of energy, with coal-fired plants providing a significant portion, alongside growing contributions from LNG-based facilities.

How will Bangladesh’s power landscape change by 2030?

Increased share of solar: The government is aiming to raise the share of RE generation from the present minuscule 3-5% to 15-20% by 2030. To achieve this target, the government is planning to encourage setting up of smaller solar power units along with 100-megawatt (MW) projects wherever land is available. The key challenge here lies in land scarcity. Thus, local power producers are trying to make the best use of available land, a source in Bangladesh informed. The common practice now is to seek around 400 acres of land parcels for setting up 100-MW solar projects. At present, around 100 MW is seen contributed by solar/RE sources.

A few solar projects are underway. These include the Arabian Company for Water and Power Operations’ 300-MW solar power project and Sumitomo’s solar PP.

“If we consider the next 5-6 years then solar power plants will be more in focus,” a source in Bangladesh observed to BigMint.

Offshore wind project viability study underway: The country is also eying offshore wind projects but because of inadequate wind speeds in Bangladesh such projects may not be very viable. However, a feasibility study is under way for an offshore wind power project through the Bangladesh China Power Company Limited (BCPCL), a joint venture between Bangladesh’s North-West Power Generation Company (NWPGCL) and China National Machinery Import and Export Corporation.

Government halts new coal-fired plants: The government has implemented a pause on the establishment of new coal-fired power plants, with several significant ongoing projects, such as the 1200×2 MW Matarari project, the 1320×2 Rampal project, and the 1320-MW Payra power plant, discontinuing their phase two construction.

Nuclear plant on way: Bangladesh is also constructing the 3000-MW Rooppur Nuclear Power Plant (RNPP) in Pabna district — a significant infrastructure project currently underway. Once it comes into operation it will help to cover the deficit of 2,400-3,000 MW.

As per government data, an additional 6,000-7,000 MW would come in, including the nuke plant, by 2026-27.

Imports of greener source of power to increase: The government is in talks with Nepal for increasing imports of hydropower to broaden the green energy basket and help it reach closer to its emission goals. At present, Bangladesh is importing around 40 MW of hydropower from Nepal and the rest from India (700 MW from Adani Power and around 100 MW from the eastern part of India).

Outlook

Bangladesh’s power demand is expected to increase from the current levels to 33,000 MW by 2030, impelled by higher economic growth and further industrialization.

Emphasis on HSFO-based generation is likely to wane because of the higher tariffs.

Looking ahead, solar tariffs are likely to be competitive and remain contained in the range of 10-11 cents per unit since many players are jostling for space here. “The lower the tariffs quoted here, the higher the chances of receiving government approval,” informed a source in Bangladesh.

4th Bangladesh International Trade Summit

Bangladesh, a strategically significant country for Asia-Pacific, is emerging as a hotspot of growth through sustainable practices. The economic expansion is expected to encourage the participation of more global companies and attract forex for the country.

BigMint Events will be hosting the 4th Bangladesh International Trade Summit on 14-15 May 2024, at Hotel Pan Pacific Sonargaon, Dhaka, Bangladesh. The two-day conference shall bring together key stakeholders from the steel, cement, and power industries, including industry stalwarts, policymakers, traders, and investors. It shall provide a network for collaboration and an ideal platform for discussion of prevailing industry trends and challenges.