Li Shubin, Executive Vice President and Secretary General of China Waste Steel Application Association pointed out that China’s waste steel resources utilization level has achieved new breakthroughs, and the development of the “13th Five-Year Plan” of the scrap steel industry is expected to be completed two years and three months ahead of schedule. The plan proposes a scrap target ratio of 20%. Not only that, the total consumption of scrap steel, the combined consumption of scrap steel and the proportion of scrap steel application have reached the best level in China’s steel industry after the removal of large flat furnace smelting process, and it also marks the development of China’s scrap steel industry.

China’s scrap resources and consumption continue to increase steadily –

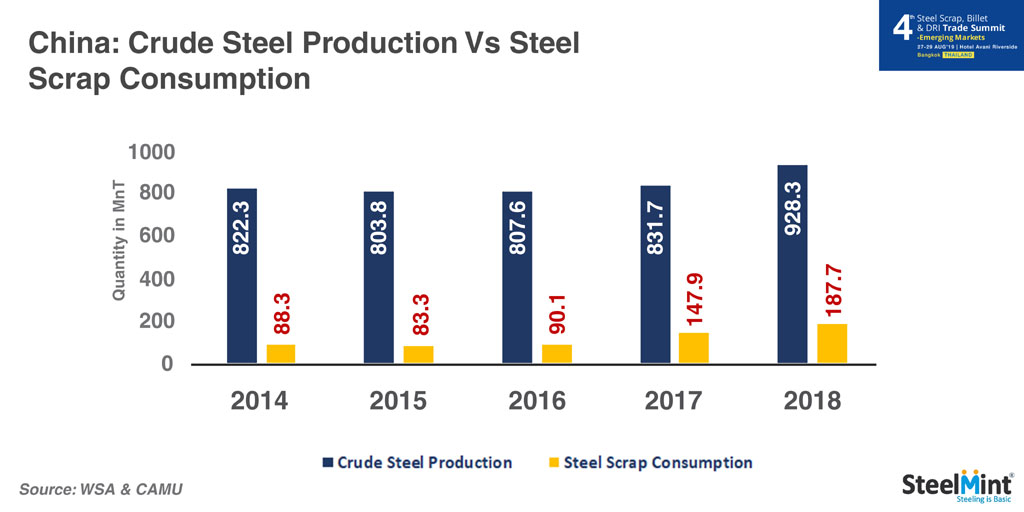

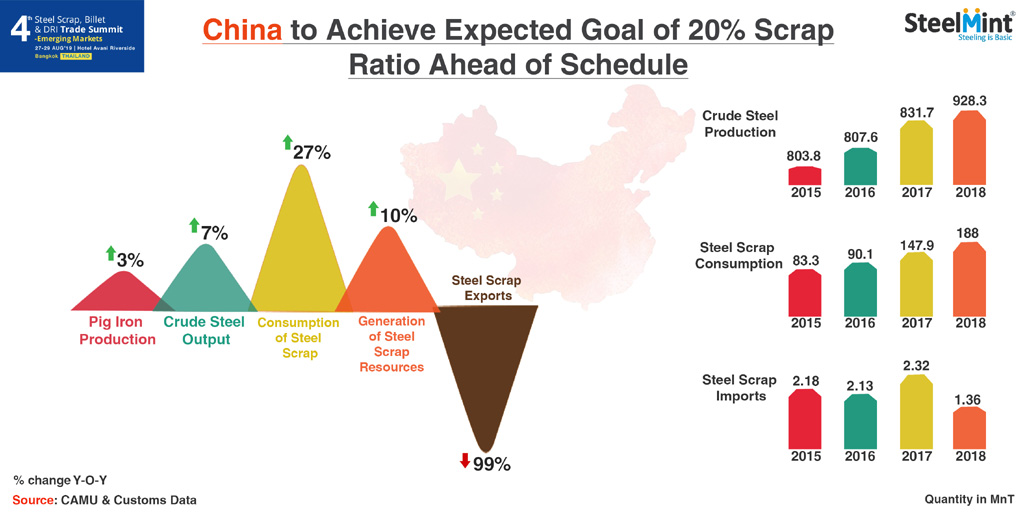

In 2018, China’s total consumption of scrap steel in the whole year was 188 MnT, an increase of 39.68 MnT, an increase of 26.9%. The scrap consumption was 202.3 kg/ton, an increase of 24.5 kg/ton, an increase of 13.8%. Among them, converter scrap consumption was 152 kg/ton, an increase of 23.8 kg/ton, an increase of 18.6%; electric furnace scrap consumption of 662.8 kg/ton, an increase of 2.2 kg/ton, an increase of 0.3%. The scrap ratio was 20.2%, an increase of 2.45% points Y-o-Y; the electric furnace steel ratio was 9.8%, an increase of 0.5% points Y-o-Y.

In the first two months of this year, the total consumption of scrap steel in the country was 29.33 MnT, an increase of 3.97 MnT, an increase of 15.6%.

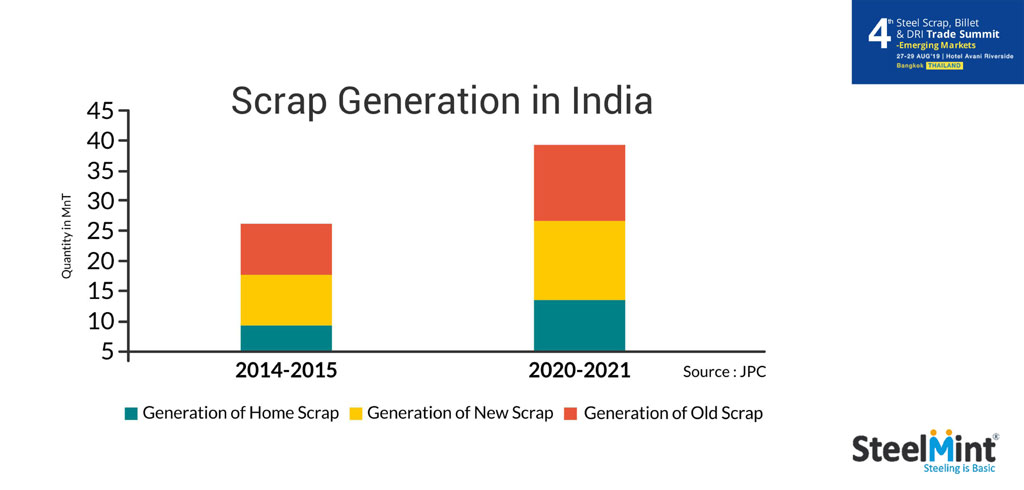

According to the statistics of the Scrap Association, the total amount of scrap steel resources generated in the country in 2018 was 220 MnT, an increase of more than 20 MnT, an increase of 10%. Iron and steel enterprises produce 50 MnT of scrap steel, accounting for 23% of total resources; social procurement of scrap steel is 170 MnT, accounting for 77% of total resources. Among them, the total consumption of scrap steel in iron and steel enterprises was 188 MnT, accounting for 85.5% of the total resources.

Problems being faced by Chinese steel scrap industry?

1. China’s waste steel recycling is still relatively low compared with the global average. There is a gap between China’s scrap ratio and the global average. It is necessary to speed up the increase of scrap ratio and increase the ratio of electric furnaces to accelerate the development of China’s scrap steel application industry.

2. The current national policy measures to use green resources for scrap steel and short-process steelmaking. It needs to be further strengthened.

3. The fiscal and taxation [2015] No. 78 document does not fully honor the preferential policies for the scrap steel enterprises. The focus should be on full use of existing capital channels such as green manufacturing, guide and encourage social capital to increase support for scrap steel application, and strengthen departments with finance and taxation. Communicate and coordinate to promote the implementation of the VAT refund and refund policy, and ensure that eligible enterprises are eligible for tax incentives.

Steel scrap prices to see no major fluctuation!

The China Iron and Steel Association predicts that steel prices will remain range bound in 2019 and there will be no major decline in scrap steel prices. The recent analysis believes that the price level of the scrap market in 2019 should fluctuate around 2,500 yuan/ton (including tax price), there will be no major decline and there will be no 2015-style decline.

Li Shubin believes that scrap prices and steel prices are linked and related to the cost of hot metal. As long as steel prices are firm, steel companies have substantial profits, scrap demand will not be greatly reduced, scrap prices will not fall sharply, but there will be no big climbs. It is reasonable for heavy scrap to float at around 2,500 yuan/ton.

What are major opportunities available for scrap processing and distribution companies?

1. 7th batch of scrap access of the Ministry of Industry and Information Technology is about to begin

2. China’s new regulations on the dismantling of scrapped cars, which will help achieve the integrated development of the scrap industry.

“Encourage scrap processing enterprises to expand and group development through mergers and acquisitions, support steel companies to lead the establishment of large-scale scrap processing and distribution enterprises, drive the green development of upstream and downstream industrial chains, and guide the rational flow of scrap steel resources.” Li shared.

To know more on Rising Importance of Steel Scrap in China, book your seat at SteelMint’s 4th Steel Scrap, Billet & DRI Summit and get a chance to hear views of Li Shubin. The conference is being organized during 27-29’th Aug’19 in Bangkok, Thailand.