Key Points of Discussion:

- Impact of war on steel capacities, production & exports

- Challenges being faced

- Market outlook for the rest of the year

Key Points of Discussion:

BIR is returning to Dubai for our World Recycling Convention (Round-Table Sessions), (16) 17-18 October 2022!

Tapping into the vast business opportunities of the Middle East was one of the many reasons why BIR decided to go back to the coveted conference destination of Dubai. This city never fails to impress and surprise, with constant innovation and superlatives while offering exquisite convention venues with all the amenities that make a business stay feel like a holiday.

Registration is now open! Register today to access the best rates & hotel availability.

The global ship-breaking or ship recycling industry has witnessed a major shift in recent years owing to environment concerns. On one hand, ship-breaking is a green process wherein a ship at the end of its life cycle is dismantled for further re-use. On the other hand, it is a complex process of dismantling that includes issues like workers’ safety and health aspects and further challenges to the environment.

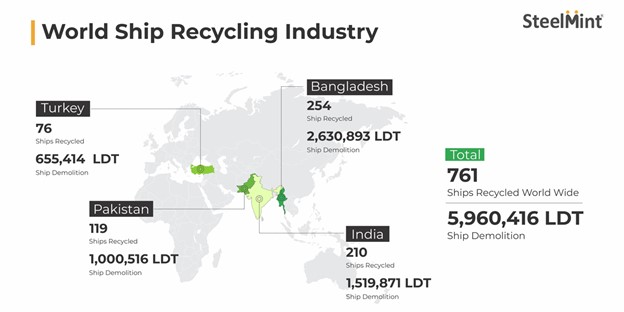

However, the ship recycling market is gaining momentum annually. A total of 761 ships were broken worldwide in CY2021 against 631 in CY2020, out of which 583 were sold to the beaches in South Asia – the world’s largest ship recycling hub in 2021.

There has been a noticeable improvement in ship-breaking volumes in 2021. Lockdown restrictions had pulled down import volumes in 2020. Diversion of oxygen for medical purposes also impacted volumes.

Ships can be classified into six broad categories like general cargo, bulk carriers, oils tankers, passengers ships, drill and war ships. The approximate age or lifespan of a ship is 25-30 years.

South Asia recycling market

South Asia has been referred to as the “World’s ship scrapping yard”, with India, Bangladesh and Pakistan collectively dismantling and processing scrapped vessels globally. India, Pakistan and Bangladesh together accounted over 80% share of the global ship recycling market in 2021.

Price trends

The average material recovery depends upon the type of material extracted from the ship. Re-rollable ferrous scrap recovery is 67%, meltable ferrous scrap around 12% whereas cast iron is 4% and non-ferrous scrap, 1%.

HKC and green recycling

Considering the hazardous nature of the industry, one key obstacle is that there is no fixed legislation to follow. The Hong Kong International Convention for the Safe and Environmentally Sound Recycling of Ships was adopted at a diplomatic conference held in Hong Kong in 2009.

The convention was adopted to ensure that ships, when being recycled after reaching the end of their functioning lives, do not create any unnecessary hazards to human health, safety and to the environment.

South Asian countries have decided to ratify and implement the Hong Kong Convention. Towards that, the relevant ministries have drafted regulations to make the ship recycling industry safe for their workers and the environment by implementing the Hong Kong Convention (HKC).

Outlook

Amid the current scenario, availability of vessels is limited and prices remain steady due to sluggish economies and low steel demand from end-user industries. As a result, market sentiments are gloomy and buyers cautious.

But ship-breaking volumes may increase in the short term due to favourable weather conditions which will support increased construction activities. It may be mentioned, a major portion of ship-recycled scrap finds its way into the construction sector.

SteelMint Events will be hosting the 3rd Steel & Raw Material Conference, Emerging Bangladesh, on 20-21 September, 2022 at Hotel Radisson Blu, Chittagong, Bangladesh. The conference will explore key issues like the country’s steel production and demand outlook, global scrap trade flow changes, especially post-the Russia-Ukraine war, the ship recycling scenario, key emerging sectors, price trends and a lot more.

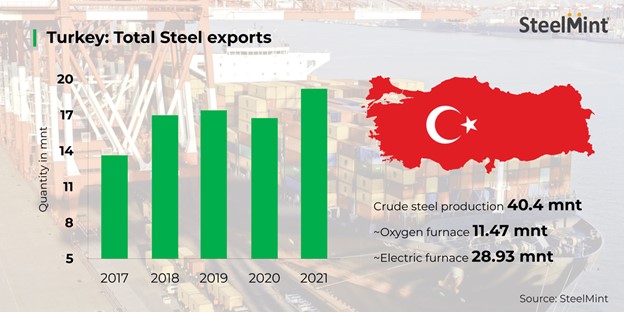

Turkiye is one of the largest ferrous scrap importing countries in the world. Other key industries that contribute to the country’s economy include textiles, chemicals, cement, motor vehicles and construction. The country provides certain leverages for international trading and is a key destination for trade between Europe and Asia.

Turkiye produced 40.4 million tonnes (mnt) of crude steel in CY 2021 out of which 11.47 mnt i.e. 28.4% was churned out from oxygen furnace (BOF) and 28.93 mnt i.e. 71.6% was produced from electric arc furnace (EAF), as per World Steel Association (WSA) report. Higher crude steel output resulted in increased scrap consumption.

Also, according to the Turkish Automotive Manufacturers’ Association (OSD), total car production in CY21 stood at 1,276,140 units wherein exports amounted to 937,005 units, marking an increase of 2% as compared to 916,538 units in CY20.

Turkiye’s scrap market in 2021

Reasons behind the rise in imports–

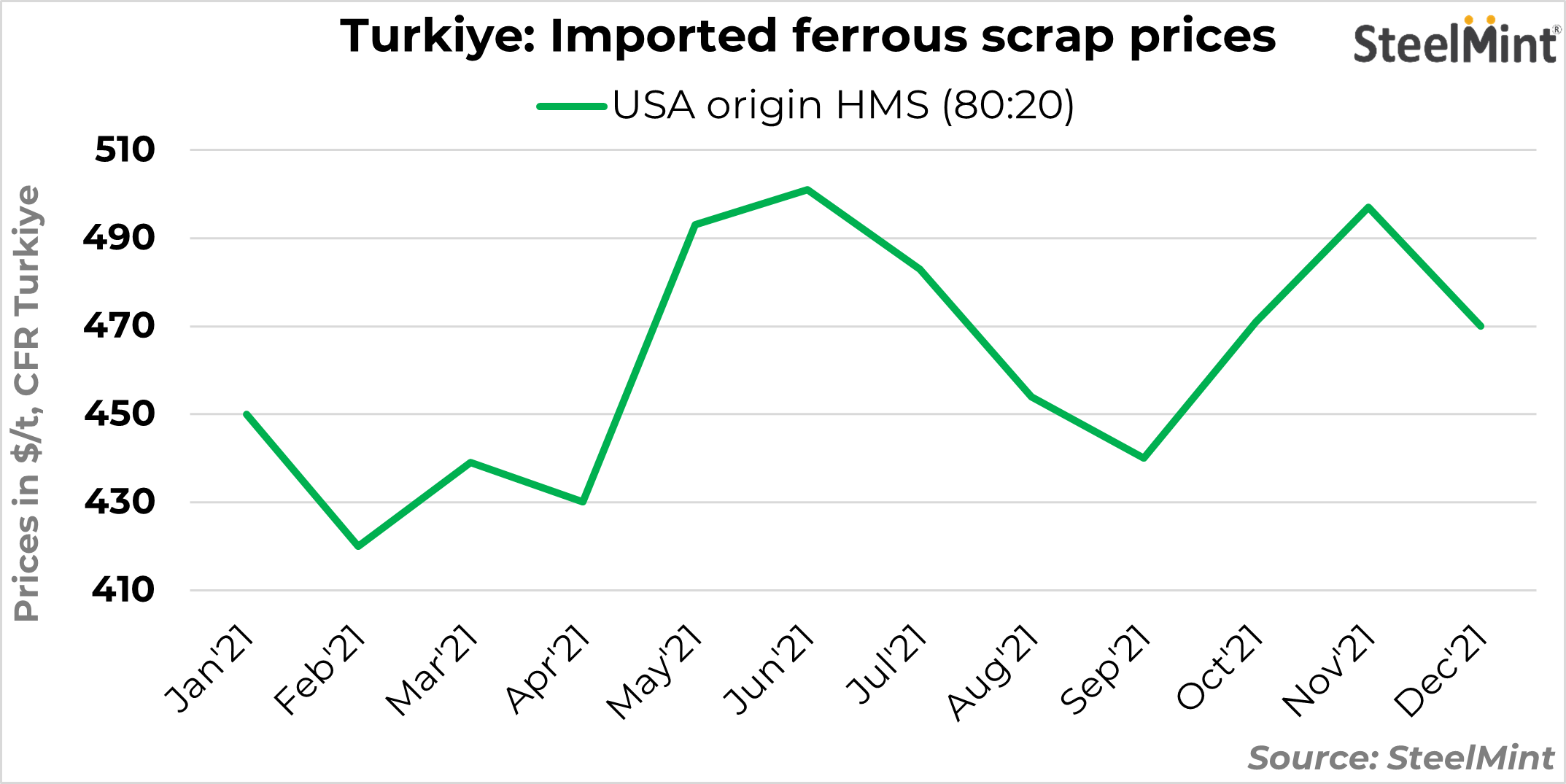

Imported scrap prices rise in CY21

SteelMint’s assessment of US-origin HMS 1&2 (80:20) stood at $459/t CFR Turkey in January-December 2021 against $291/t CFR in January-December 2020, up by around $168/t CFR Turkey y-o-y.

Prices surged as Lira eroded against the dollar to settle at TRY 13.31 in 2021 which was at 7.37 towards the end of 2020. The volatile market situation and a sharp fluctuation in the national currency put pressure on steel mills to lower their local scrap prices in 2021. Also, sluggish domestic and overseas demand, especially from China amid the winter months kept Turkish market under pressure.

Hassles in scrap market:

Way forward:

The input costs of Turkish steel mills are anticipated to increase further after the country’s Energy Market Regulatory Authority elevated electricity prices for industrial use by 50% on 31 August 2022. State gas distributor Botas also raised natural gas prices for industrial use by 50.8% from September 2022. This may lead in Turkish steel mills opting for production cuts or lift prices despite the sluggish market as their margins are lower.

SteelMint Events will be hosting the 3rd Steel & Raw Material Conference, Emerging Bangladesh, on 20-21 September, 2022 at Hotel Radisson Blu, Chittagong, Bangladesh. The conference will explore key issues like the country’s steel production and demand outlook, global scrap trade flow changes, especially post-the Russia-Ukraine war, the ship recycling scenario, key emerging sectors, price trends and a lot more.

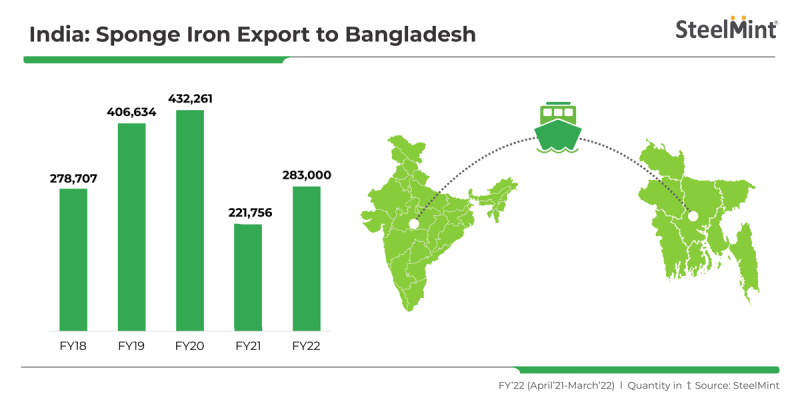

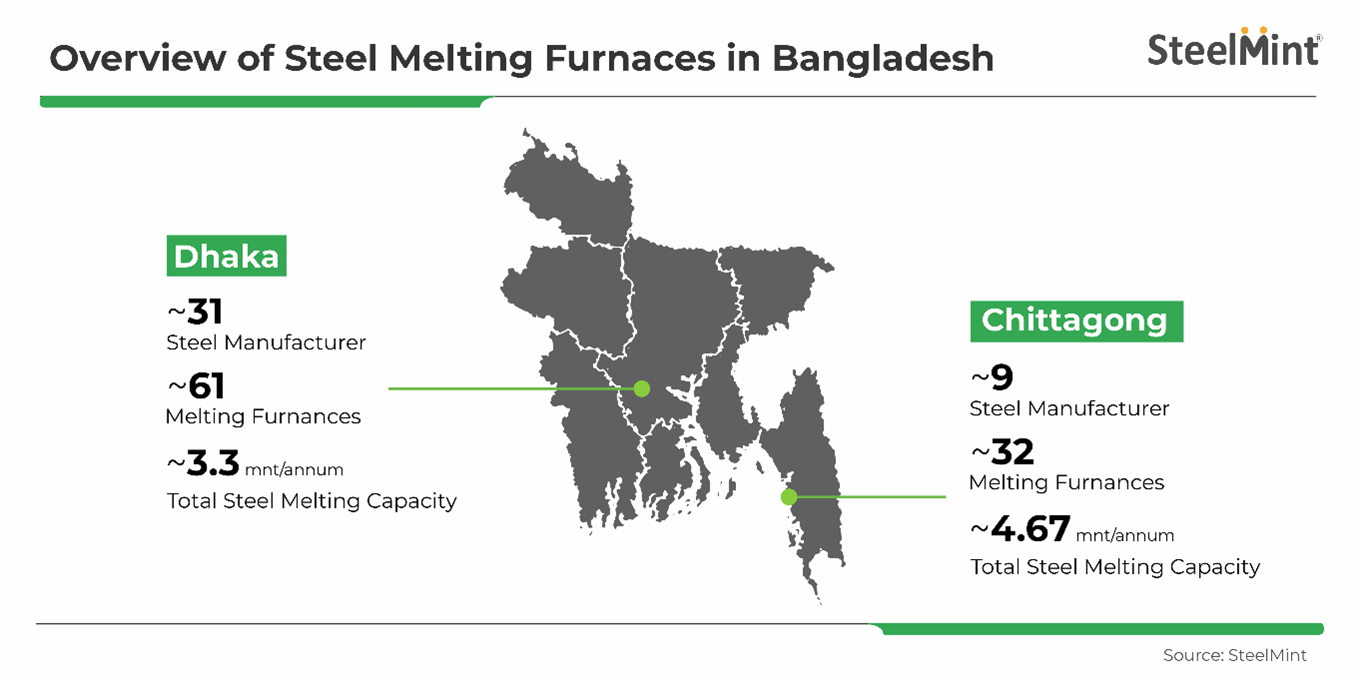

Sponge iron imports by Bangladesh from India stood at 283,000 tonnes (t) in FY’22 (April’21-March’22). Although Bangladesh’s imports increased sharply from FY’21, volumes were still lower compared to the previous couple of fiscals. Imports, however, are expected to edge up in the coming time on account of rising steel melting capacities in Bangladesh and infrastructure projects in the pipeline.

Notably, Bangladesh’s financial year starts on 1 July and ends on 30 June. The country’s sponge iron imports were recorded at a meagre 221,756 t in the Indian fiscal year 2021 (FY’21) due to the impact of the COVID-19 pandemic. Meanwhile in the first six months (January-July) of CY’22 the country imported 443,092 t of sponge iron from India, indicating a surge in demand. However, due to LC issues and the liquidity crisis buyers booked limited material during June-July.

Bangladesh accounts for 41% of Indian sponge exports: Bangladesh has a share of 41% in India’s total sponge exports, with export volumes in FY’22 being recorded at 690,287 t. While Nepal accounts for the largest share – 53% – of India’s exports, Bhutan holds a share of 5%.

Bangladesh’s sponge import prices: Imported sponge iron prices to Bangladesh stood at an average level of $494/t CNF Chittagong in FY’22.

Market updates

As many steel manufacturers in Bangladesh are planning to expand their steel capacities, DRI imports from India are poised to rise further.

To know more on Bangladesh’s sponge iron imports, book your seat at 3rd Steel & Raw Material Conference, Emerging Bangladesh on 20-21 September, 2022 at Hotel Radisson Blu, Chittagong, Bangladesh, and get a chance to hear renowned industry participants from across the globe on “How are Indian mills managing feed mix of Scrap/DRI/Pig Iron in Induction Furnaces (IF)”.