Vehicle recycling is gaining momentum in India. The country’s first vehicle recycling facility was formed by a joint venture between Mahindra Accelo and MSTC Ltd, a Government of India enterprise. SteelMint, caught up with Mr. Vijay Arora, Vice President, Strategy, Operations and Business Development, Mahindra Group Accelo, India, to learn about his views on the present and future vehicle recycling scenario in India. Below are edited excerpts from the interview:

1. How do we see the changing scenario in the Auto recycling industry in India? What could be the growth potential of this sector in the coming years?

Recycling is the need of the hour. Talking about vehicle recycling, almost 50,000 new vehicles are put on Indian roads every day. If we take the average life of a vehicle to be 15 years, there are about 26 million end-of-life vehicles in India currently. And this is expected to increase up to 42 million by 2025.

These numbers are testimony to the tremendous growth potential and necessity for the recycling industry. The market is showing a positive transition as awareness about the benefits of recycling as well as disadvantages of doing it in an unscientific manner are increasing. Deploying state-of-the-art recycling technologies for sorting waste will further improve recycling.

Awareness about the fact that ‘traditional recycling methods are not sufficient for quality recycling’ will offer great possibilities in this sector in the coming years. Even the government is taking note of these things.

2. What are the present developments of Mahindra CERO’s ELV processing facility in Noida which was set up in co-operation with MSTC?

We have set up India’s first state-of-the-art facility at Greater Noida for de-polluting, dismantling, bailing and shearing end-of-life vehicles (ELVs). We operate with an objective of zero tolerance towards unscientific methods of treating ELVs. We have the capability to recycle cars, trucks and buses, 2-wheelers and industrial scrap. We are shortly starting operations at our second collection-cum-dismantling centre at Chennai and will be opening 3 more centres this year.

3. What are your views on implementation of the ‘Vehicle Recycling Policy’? By when do you feel it’s impact is likely to be felt?

The Vehicle Recycling Policy, which would make scrapping of end-of-life vehicles mandatory, will have its impact in a big way. The impact would be visible once the policy is in place, but one needs to keep in mind that there exists an elaborate unorganised sector that has grown and become an established system in the country. It will take considerable time for the mind-set to change and an organised recycling industry to become effective.

4. What is the progress at the other 3 auto recycling facilities which were planned earlier across India? What are the other future initiatives in the pipeline?

We are starting our operations in Chennai by the end of this quarter. Post-that, we will set up 4 more facilities at Bengaluru, Kolkata, Mumbai/Pune and Hyderabad. We plan to be present in 25 locations in the next 2-3 years, covering all major catchment areas. ELV shredding is also planned and will come up as soon as we have more clarity on the policy.

5. A few other major companies in India are also eyeing an entry into the recycling space. How is Mahindra likely to withstand this competition?

Setting up state-of-the art recycling infrastructure pan-India and inclusion of the informal sector within CERO will be Mahindra’s differentiating factor. We would focus on our USPs of utilizing latest recycling technology, developing partnerships with all stakeholders and providing hassle-free process for our customers in scrapping their vehicles by strictly following environmental norms during the process.

6. How much steel scrap is expected to be generated domestically and how much scrap will India import once these shredding plants come into operation?

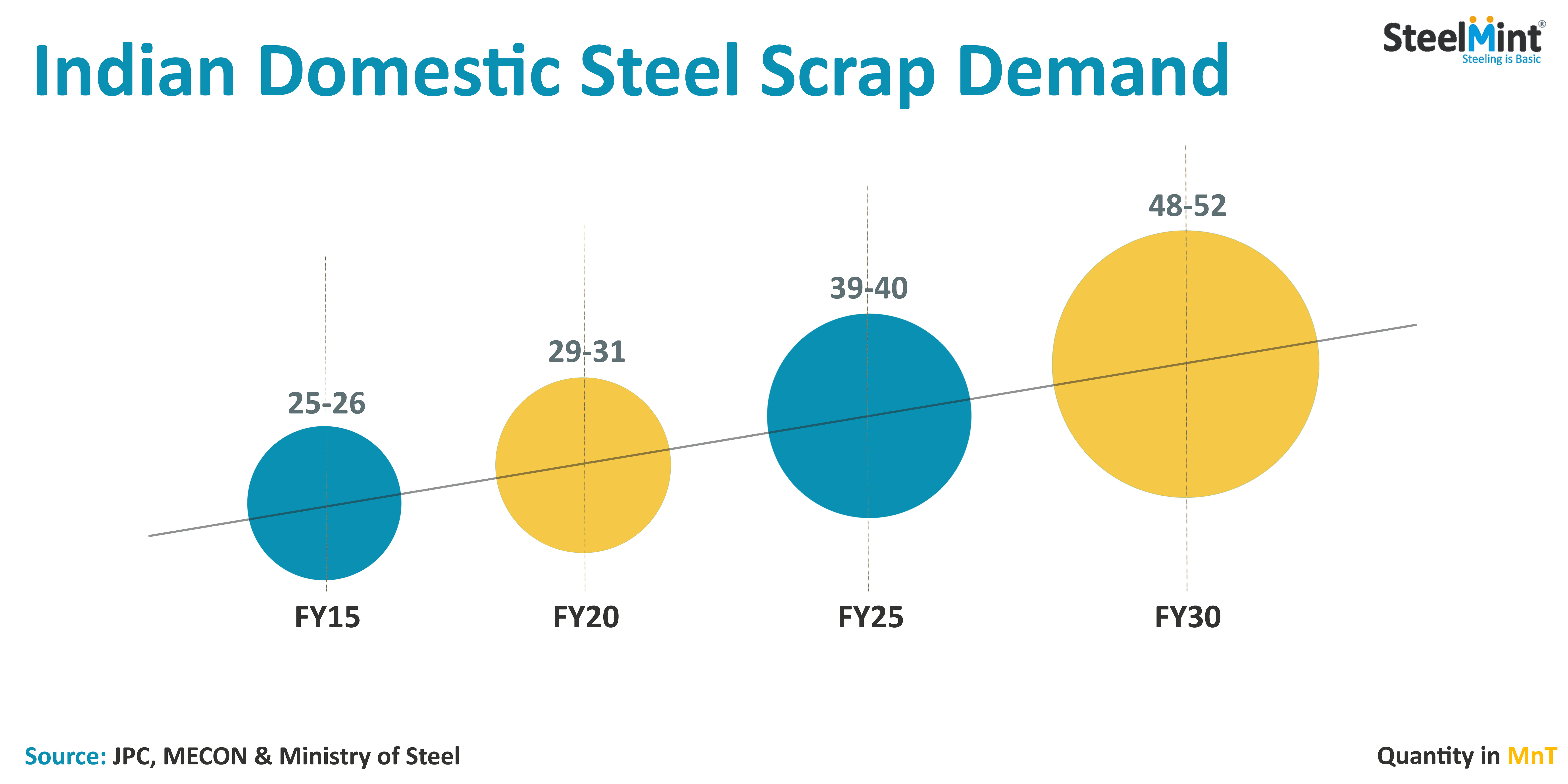

In 2015, India’s domestic demand for steel scrap was about 26 million tonnes (MnT) while domestic supply was about 19-20 tonnes (MT), leading to imports of about 7-8 MnT. By 2030, this demand is expected to grow to 45-50 MnT. Production of steel scrap domestically will help in reducing India’s dependence on steel scrap imports, thereby saving the country’s precious foreign exchange reserves.

7. What are the challenges this industry is facing and how can these be fixed from your point of view?

All the stakeholders need to play some role for this industry to prosper. Currently, ELV owners are not aware of the ill-effects of running their old vehicle. Those who want to scrap it, do not have proper channels to do so. We have issues of lack of rules and regulations pertaining to deregistration, GST etc. A government policy that makes scrapping of vehicles mandatory and provides tax incentives or investment promotion subsidies will help formalise this sector. Secondly, following best practices of European and other developed countries of formulating an Extended Producer Responsibility (EPR) for the original equipment manufacturers (OEMs), which will also help as they will be then integrated into the ecosystem

In order to know more about India’s vehicle recycling, book your seat at SteelMint’s 4th Steel Scrap, Billet & DRI Trade Summit and get a chance to hear insights from Mr. Vijay Arora. The conference is being organised during 27-29th August, 2019 in Bangkok, Thailand.